15 Best best burial insurance for seniors Bloggers You Need to Follow

The Basic Principles Of What Is Auto Insurance? Affordable Financial Loss Protection

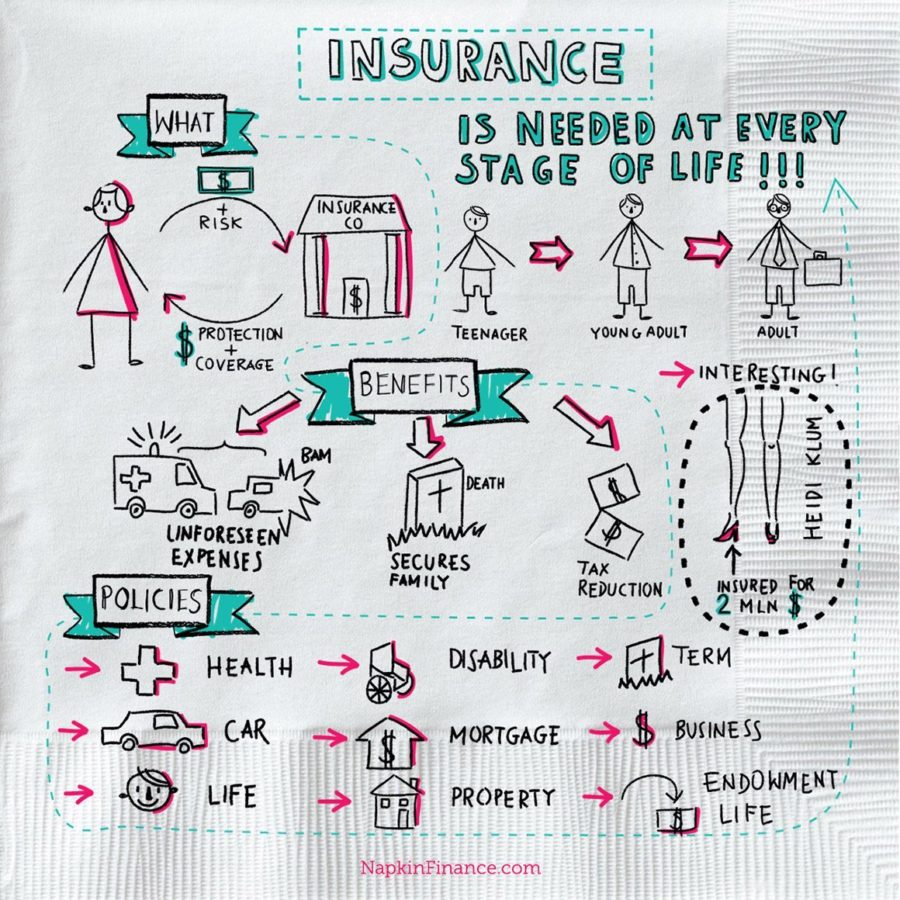

Equitable transfer of the threat of a loss, from one entity to another in You can find out more exchange for payment A marketing poster for a Dutch insurance provider from c. 19001918 illustrates an armoured knight. Insurance coverage is a means of protection from monetary loss. It is a type of danger management, mostly utilized to hedge against the risk of a contingent or unpredictable loss.

A person or entity who purchases insurance is called an insured or as an insurance policy holder. The insurance deal includes the insured presuming a guaranteed and understood reasonably little loss in the form of payment to the insurer in exchange for the insurance provider's pledge to compensate the insured in case of a covered loss.

Getting The What Is Insurance? Meaning, Types, And Terms - Getinsurance To Work

The insured gets a agreement, called the insurance plan, which details the conditions and scenarios under which the insurer will compensate the guaranteed. The amount of cash charged by the insurance company to the insurance policy holder for the coverage stated in the insurance plan is called the premium. If the insured experiences a loss which is possibly covered by the insurance coverage, the insured sends a claim to the insurer for processing by a claims adjuster.

Merchants have looked for methods to reduce dangers since early times. Envisioned, Governors of the Red wine Merchant's Guild by Ferdinand Bol, c. 1680. Methods for transferring or dispersing threat were practiced by Chinese and Babylonian traders as long ago as the 3rd and 2nd centuries BC, respectively. Chinese merchants taking a trip treacherous river rapids would redistribute their items throughout numerous vessels to restrict the loss due to any single vessel's capsizing.

What Is An Insurance Premium? Definition And Cost, Explained ... Fundamentals Explained

1750 BC, and practiced by early Mediterranean sailing merchants. If a merchant got a loan to money his delivery, he would pay the lender an extra sum in exchange for the lending institution's warranty to cancel the loan needs to the shipment be taken, or lost at sea. Circa 800 BC, the occupants of Rhodes developed the 'basic average'.

The ancient Greeks had marine loans. Cash was advanced on a ship or freight, to be paid back with big interest if the voyage flourish, however not repaid at all if the ship be lost, the interest rate being made high enough to pay not only for making use of the capital, however for the risk of losing it (completely explained by Demosthenes).

The Ultimate Guide To What Is Insurance? - Money Advice Service

The direct insurance of sea-risks for a premium paid separately of loans began, as far as is known, in Belgium about A.D. 1300. Different insurance coverage agreements (i.e., insurance plan not bundled with loans or other kinds of contracts) were developed in Genoa in the 14th century, as were insurance swimming pools backed by pledges of landed estates.

These new insurance coverage contracts allowed insurance to be separated from investment, a separation of functions that first proved useful in marine insurance. The earliest recognized policy of life insurance coverage was made in the Royal Exchange, London, on the 18th of June 1583, for 383, sixes. 8d. for twelve months, on the life of William Gibbons.

Rumored Buzz on What Is Insurance? Definition And Meaning ...

Property insurance as we know it today can be traced to the Terrific Fire of London, which in 1666 feasted on more than 13,000 homes. The disastrous effects of the fire converted the advancement of insurance coverage "from a matter of convenience into one of seriousness, a modification of viewpoint reflected in Sir Christopher Wren's inclusion of a site for 'the Insurance Workplace' in his new prepare for London in 1667." A variety of tried fire insurance coverage schemes came to absolutely nothing, however in 1681, financial expert Nicholas Barbon and eleven associates established the first fire insurance provider, the "Insurance Coverage Office for Houses", at the back of the Royal Exchange to insure brick and frame houses.

At the very same time, the very first insurance plans for the underwriting of service ventures appeared. By the end of the seventeenth century, London's development as a centre for trade was increasing due to the demand for marine insurance coverage. In the late 1680s, Edward Lloyd opened a coffee home, which ended up being the meeting place for celebrations in the shipping market wanting to guarantee cargoes and ships, including those happy to underwrite such endeavors.

The Facts About How Insurance Works - Mental Health America Revealed

/insurance-faa9df3f80274172970efdd638aca3cb.jpg)

The very first life insurance coverage policies were secured in the early 18th century. The first company to use life insurance coverage was the Amicable Society for a Continuous Guarantee Workplace, established in London in 1706 by William Talbot and Sir Thomas Allen. Upon the exact same concept, Edward Rowe Mores developed the Society for Equitable Assurances on Lives and Survivorship in 1762.

5 Vines About senior burial insurance That You Need to See

The Ultimate Guide To What Is Insurance? - Facts On Insurance

If the Insured has a "reimbursement" policy, the insured can be needed to pay for a loss and after that be "reimbursed" by the insurance carrier for the loss and expense costs consisting of, with the authorization of the insurance provider, claim expenditures. Under a "pay on behalf" policy, the insurance carrier would safeguard and pay a claim on behalf of the guaranteed who would not run out pocket for anything.

Under an "indemnification" policy, the insurance carrier can generally either "reimburse" or "pay on behalf of", whichever is more beneficial to it and the guaranteed in the claim managing procedure. An entity looking for to transfer danger (a person, corporation, or association of any type, and so on) becomes the 'insured' celebration once threat is presumed by an 'insurer', the guaranteeing party, by means of a agreement, called an insurance coverage.

An insured is hence said to be "indemnified" versus the loss covered in the policy. When insured celebrations experience a loss for a defined hazard, the protection entitles the insurance policy holder to make a claim versus the insurance company for the covered quantity of loss as specified by the policy. The cost paid by the guaranteed to the insurance company for assuming the risk is called the premium.

See This Report on Homeowners Insurance: What It Is And What You can find out more It Covers ...

So long as an insurance provider keeps sufficient funds reserved for awaited losses (called reserves), the remaining margin is an insurer's revenue. Policies usually consist of a variety of exclusions, including normally: Insurance can have numerous impacts on society through the manner in which it alters who bears the expense of losses and damage.

Insurance coverage can affect the likelihood of losses through ethical danger, insurance scams, and preventive steps by the insurer. Insurance scholars have typically utilized ethical threat to refer to the increased loss due to unintentional negligence and insurance scams to refer to increased danger due to intentional recklessness or indifference.

While in theory insurers could encourage financial investment in loss reduction, some analysts have argued that in practice insurers had historically not strongly pursued loss control measuresparticularly to avoid catastrophe losses such as hurricanesbecause of issues over rate decreases and legal battles. However, since about 1996 insurance providers have begun to take a more active function in loss mitigation, such as through building regulations.

The 9-Second Trick For How Insurance Works Abi

Nevertheless, in case of contingency insurance coverages such as life insurance coverage, dual payment is allowed) Self-insurance circumstances where risk is not moved to insurer and exclusively maintained by the entities or individuals themselves Reinsurance circumstances when the insurance company passes some part of or all threats to another Insurance company, called the reinsurer Mishaps will happen (William H.

Collection EYE Film Institute Netherlands. Insurance companies may utilize the membership service design, gathering premium payments periodically in return for on-going and/or compounding advantages offered to insurance policy holders. Insurance companies' company design aims to collect more in premium and investment income than is paid out in losses, and to likewise provide a competitive cost which customers will accept.

Insurance providers generate income in two methods: Through underwriting, the process by which insurers pick the threats to insure and decide how much in premiums to charge for accepting those risks, and taking the brunt of the danger should it come to fruition. By investing the premiums they gather from insured parties The most complex element of guaranteeing is the actuarial science of ratemaking (price-setting) of policies, which utilizes stats and possibility to approximate the rate of future claims based upon an offered threat.

The 4-Minute Rule for What's Medicare? - Medicare

At one of the most basic level, preliminary rate-making involves looking at the frequency and intensity of insured dangers and the anticipated typical payment arising from these dangers. Thereafter an insurance provider will collect historical loss-data, bring the loss data to present value, and compare these prior losses to the premium gathered in order to examine rate adequacy.

Ranking for different threat qualities involves - at the many standard level - comparing the losses with "loss relativities" a policy with twice as numerous losses would, therefore, be charged twice as much. More intricate multivariate analyses are sometimes utilized when several attributes are involved and a univariate analysis might produce puzzled results.

Upon termination of a provided policy, the amount of premium gathered minus the quantity paid out in claims is the insurance company's underwriting revenue on that policy. Financing performance is determined by something called the "combined ratio", which is the ratio of expenses/losses to premiums. A combined ratio of less than 100% shows an underwriting profit, while anything over 100 suggests an underwriting loss.